Pet Insurance: What New Pet Owners Need to Know

Pet Insurance: What New Pet Owners Need to Know

With pet ownership on the rise, many new pet parents are considering pet insurance for the first time. I answer some common questions in the blog post below.

What insurance coverage does my pet need?

First ask yourself what you want the insurance to cover. Do you want coverage for annual wellness care or accident-only care – or both? What about other recurring care, like tooth cleaning? Your financial situation can be a good guide: if you have a large rainy-day fund saved up, you could consider skipping the accident-only coverage. If your budget is tighter, an all-inclusive plan can offer financial protection if your pet is ever sick or injured. Once you have answered these questions, you can narrow your search and review policies that meet your needs.

Some employers offer pet insurance as part of their benefits package – check with your employer to see what might be available.

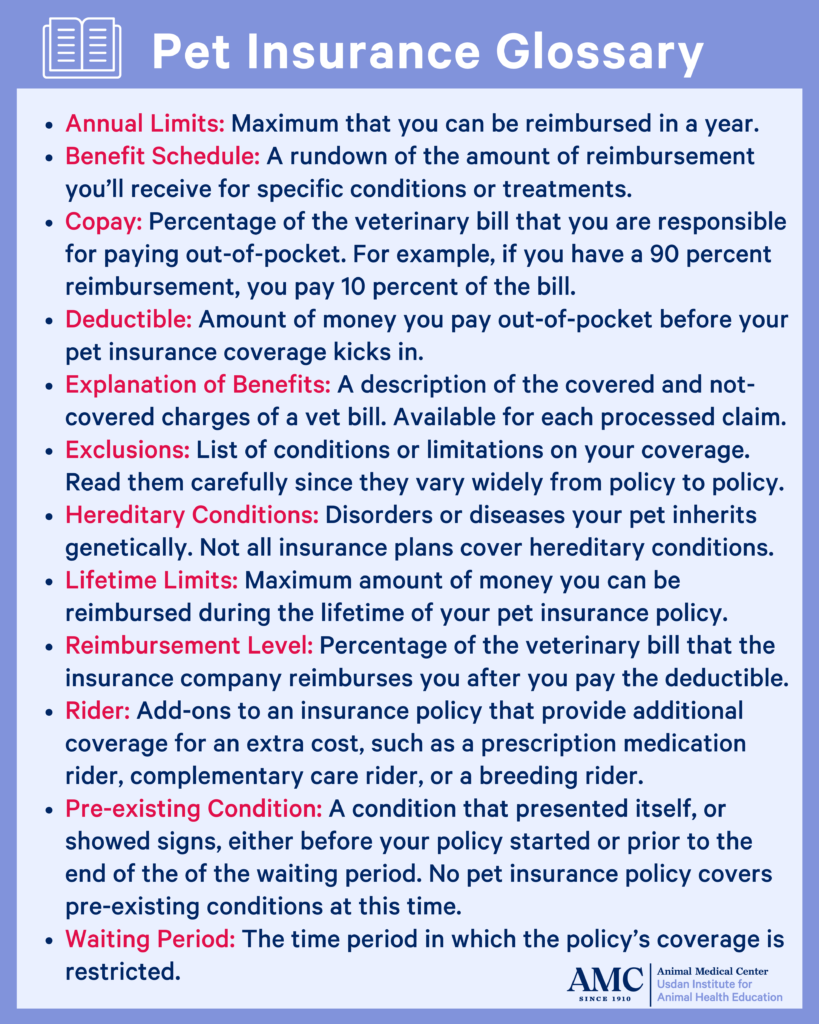

What is a deductible?

Most insurance policies have a deductible, which is the amount you must pay before the insurance “kicks in” and begins contributing to the cost of your pet’s care. A higher deductible will mean lower monthly costs, and a lower deductible will mean higher monthly costs. Do the math and see what’s right for your family, depending on your coverage needs and financial situation.

Also be sure to check and see if the deductible is per year or per condition.

Example 1: Your pet has an ear infection and gets bladder stones. Is there one deductible for both problems (obviously you will meet the deductible quickly), or do you have to meet the deductible for each problem separately? Meeting two deductibles will cost you more out of pocket.

Example 2: Your pet has cancer that requires regular visits to the veterinarian. With a lifetime per condition deductible, you would only have to meet the deductible for that condition one time, as opposed to paying out of pocket to meet an annual deductible each year.

Additionally, some insurance policies will exempt certain treatments from their deductible, meaning they will always reimburse you for that treatment, whether you’ve met the deductible or not. This is common with preventive healthcare like heartworm or flea and tick medications, if that is part of your policy.

How do I use a pet insurance policy?

Once you have pet insurance and you visit a veterinarian for a covered service, you will pay the veterinarian for their care then submit the paperwork to your insurance company to be reimbursed.

This is different from human health insurance, which typically pays the healthcare provider directly and you pay any residual costs not covered.

Do I need to check to see if my veterinarian accepts my insurance plan?

In short, no. Because you pay your veterinarian directly and get reimbursed by your insurance company later, it is not necessary for your veterinarian to have an established relationship with your insurance company. Of course, there can always be exceptions, so call your veterinarian’s office to double check before purchasing insurance coverage.

Do pet insurance policies over preexisting conditions?

The short answer is no. I recommend getting insurance early since a puppy or kitten is less likely to have a preexisting condition. If you are insuring an older dog, the insurance company will ask for medical records to determine if there is a preexisting condition or clinical signs of a preexisting condition.

Some insurance policies consider “repeat offender” accidents as a preexisting condition. For example, if your dog eats something that needs to be removed with endoscopy or surgery and it happens a second time, the procedure might not be covered.

Other Important Questions to Ask of Your Pet Insurance

- Does the policy cover a pet at any age? Does the policy run out when your pet hits a certain age? Can the policy take effect when your new puppy is born? Does the premium increase as your pet ages?

- Does the policy cover examination fees?

- Is there a limit on primary care visits or number of vaccinations per year?

- Does the company have a bilateral exclusion clause? For example, if your dog has one cruciate ligament rupture and needs surgery to repair it, will the insurance cover the cruciate ligament repair on the other leg?

- Does the company have a breed exclusion? If you are a purebred dog owner, know what diseases run in your breed. You can find this information by looking up the breed club’s website and finding the health information on your breed. Once you know that information, check how the policy handles those specific diseases.

Final Pet Insurance Thoughts

- Before you embark on costly procedures or treatments, ask your veterinarian for an itemized estimate and submit that estimate to your insurance company for preapproval. In some cases, this will allow the company to pay the hospital directly rather than you paying out of pocket and being reimbursed.

- Learn the company’s website. Some are very user friendly and allow electronic submissions of invoices by the owners or the veterinarian’s office. Others are not as tech savvy.

- Does the policy have a cap? Lifetime? Annual? Based on a diagnosis?

- Read the fine print before you agree to any non-urgent treatments. For example, if your pet needs physical therapy after surgery, will the insurance company pay for one session at a time or will it pay for a package of 10 visits prescribed by your veterinarian?

For more information on pet insurance, read the information in our Pet Health Library or read my interview with Newsweek here.

About the Author

Related Posts

-

Traveling with PetsJune 04, 2014

Resources for Summer Pet Travel

Learn More -

CatsOctober 02, 2013

How to Recognize a Sick Cat

Learn More -

Pet InsuranceAugust 21, 2013

Pet Insurance: FAQ from The AMC

Learn More